Synopsis

Until recently, plan sponsors have relied on a calendar of communication campaigns directed to all participants regardless of need to fulfill their fiduciary responsibility. To demonstrate fiduciary responsibility in 2021, plan sponsors still need to deliver all participants the same experience but also to modulate the experience according to the needs of each” just-in-time”, triggered by specified “events”. “On-demand communications” are defined as delivered to the recipient as soon as or whenever required.

Big Picture

The purpose of defined contribution plans is to help employees prepare for retirement. The goal of employee communication, education, counseling, and coaching is always to convince participants to participate in the plan, save more, consider the allocation of assets, consolidate all their retirement assets, and set up a plan draw-down strategy.

Historically, participant communication and education programs were delivered to all participants equally regardless of relevance. The general blanketing of information sent en masse to all participants regardless of relevance can in fact, do more harm than good. E.g., a communication about loans sent to all participants could result in increased loan utilization. A more effective way to mitigate loan initiation would be a targeted communication to participants with a history of borrowing from their retirement plan, just before they are about to take a loan (e.g., small loans around the Holidays) demographics by age, by account balance, by retirement readiness level, by loan utilization, by contribution level, by employment status, by marital status, etc. are critical data points.

PARTICIPANTS ARE LOOKING FOR IMMEDIATE HELP – WHAT DO I DO NOW? WHAT’S THE NEXT STEP? WHAT BUTTON DO I CLICK?

Effective communication is timely and relevant. This is complicated by the retirement plan paradigm. To be effective, to get attention, information needs to be delivered just in time – when they need it, delivered just at that moment when it is needed. To maximize effectiveness of communications, the message must be delivered to the participant at the right time and the most effectual way. Gone are the days of campaigns directed to all participants.

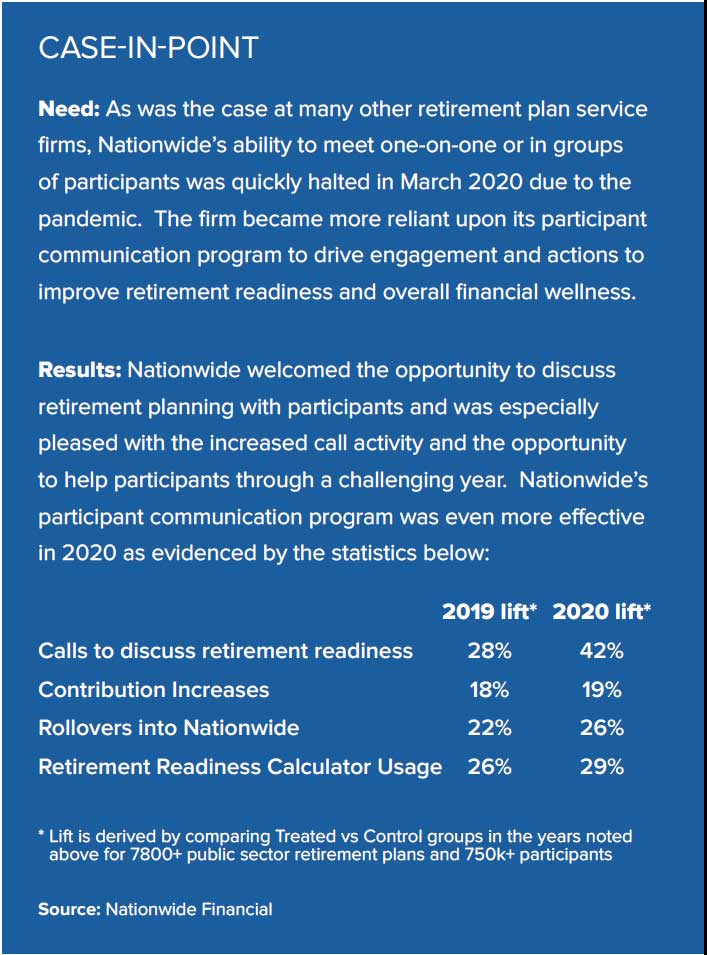

Communications need to be targeted to specific participants for specific situations. This Is becoming more often possible with the advent of data, data aggregation, marketing technology, mobile devices and communication/education programs designed to be more pertinent to individual situations. For this reason, usage of information skyrocketed and the behavior of 401(k) plan investors improved to the point that retirement readiness and the overall financial wellness of participants improved through a difficult period. Carrying forward this regimen of communication through the entire decade is the best course of action for employers who sponsor a 401(k) plan and their retirement plan service providers.

THE SMART PHONE, APPLICATIONS, AND THE IMMEDIACY THOSE DEVICES AND TOOLS BRING WILL HAVE A BIG EFFECT IN GETTING PARTICIPANTS WHERE THEY NEED TO BE.

The dramatic increase in usage of apps like DoorDash, Amazon, Facebook, Instagram, WhatsApp and others has encouraged a culture of enabling a sense of immediate gratification while demonstrating that more and more Americans are relying on their mobile devices for much more than talking, taking a selfie or posting a TikTok video.

The facility with things digital has led many savers to rely on their mobile device to access information about their retirement plans. Most service providers have released apps as part of their digital participant experience. One firm reported that mobile app usage skyrocketed, moving the needle from 64% month-to-month usage to 94%-96%. A high percent of deferral changes and other decisions recorded over the period were made by mobile app users in the mobile app offered by the firm.

Lessons Learned During The Pandemic

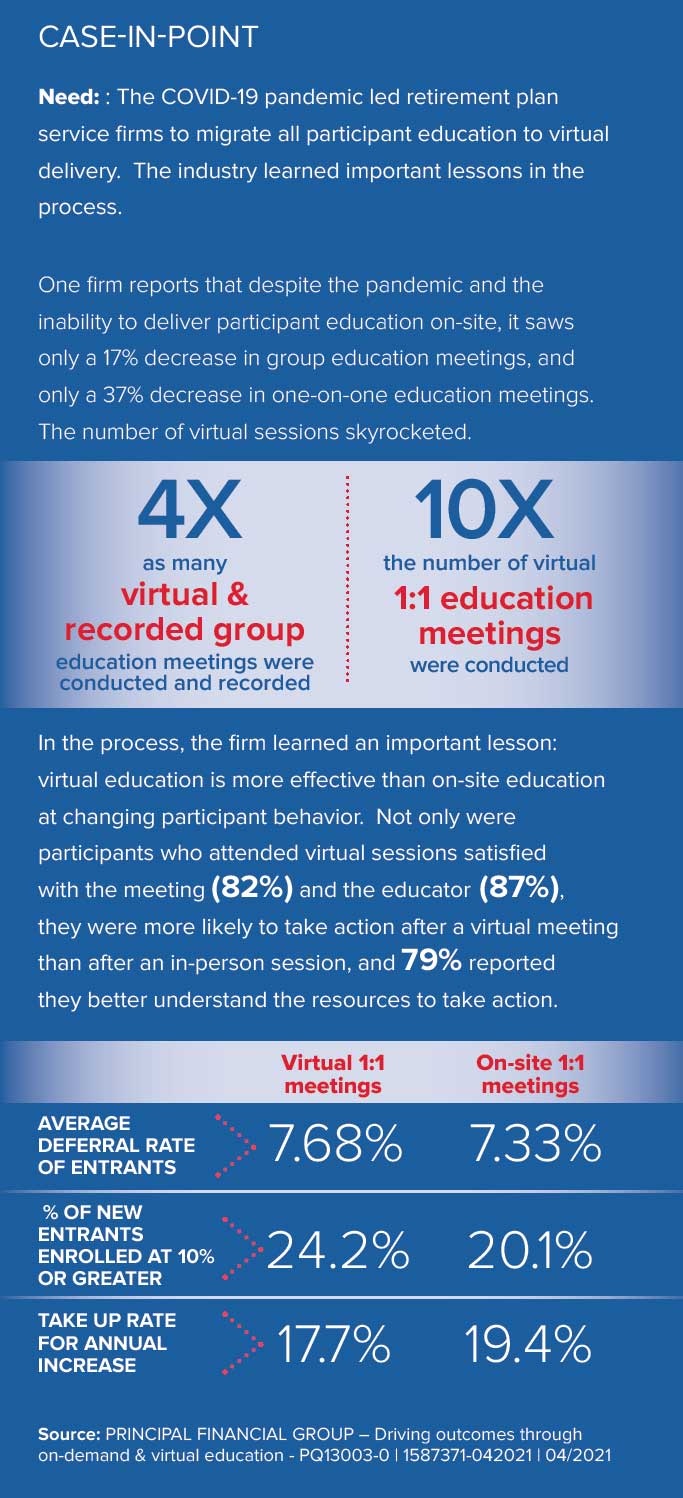

As the coronavirus pandemic unfolded, accompanied by market turbulence, timing of communications was critical. It became clear that savers want to receive information from a trusted source; they also want to receive information just-in-time, when needed. For this reason, 401(k) plan firms shifted from scheduled in-person group meetings to a more self-service online delivery model, directing participants to content relevant to their specific situation at the time of need. Results were spectacular.

Intelligent Participant Communication

Most retirement plan service providers leverage an intelligent platform to deliver and direct communication and education to participants when and how they need it. The intelligence of the platform is not necessarily “artificial”, but it needs to be deliberate – dripping content from the library of Financial Wellness information to specific participants as they need it. Instead of asking for a calendar of campaigns – smart sponsors ask for some control over the experience – ask what levers are available on the plan sponsor workstation to trigger communication A or communication B for specific events. The plan sponsor has an opportunity to be more prescriptive while engaging with their service provider. It is the fiduciary responsibility for plan sponsors to design a participant journey that is suitable for their participant population through the stages of their work life.

WHAT IS THE PURPOSE OF THIS COMMUNICATION? ASK THE QUESTION FOR EVERY COMMUNICATION AND MAKE DISTRIBUTION DECISIONS ACCORDINGLY.

The participant is now comfortable with virtual access to information – whether it’s ordering dinner, banking, shopping for supplies, or watching a video on how to change a tire or bake a cake. The real world and the retirement plan world are not distinct and separate from the participant lens. There is an increasing need for availability of access to information and transaction capabilities 24x7. And the participant is growing accustomed to controlling that access.

NEW APPROACHES TO COACHING AND TRAINING

What about an approach that expands coaching to the virtual world? Almost 5 billion videos are watched on Youtube every single day. The average mobile viewing session lasts more than 40 minutes. This is up with more than 50% year-over-year. More than half of YouTube views come from mobile devices. * If the video is done well, interested parties will watch. Instructional YouTube videos are like on-demand coaching sessions; coaxing the viewer to try to fix the doorknob, make sushi or even tie a bow tie. What does “in person” mean? Is it real-time human interaction or is it a video with a specific education or information goal available when and how the participant desires? It is an avenue worth exploring in the participant education arena.

Available content could extend from the expected investment or plan related detail to access to “YouTube” videos of practical instructions on filling out a beneficiary form, or QDROs. The objective is to give participants the feel of a one-on-one interaction with an instructor or coach—on their schedule! Search engine on key words to look through a library of content for participants in video format – so participants get the feel of a one-on-one interaction with an instructor/coach without the in-person live interaction.

The Benefits of Communicating Just-in-Time and On-Demand

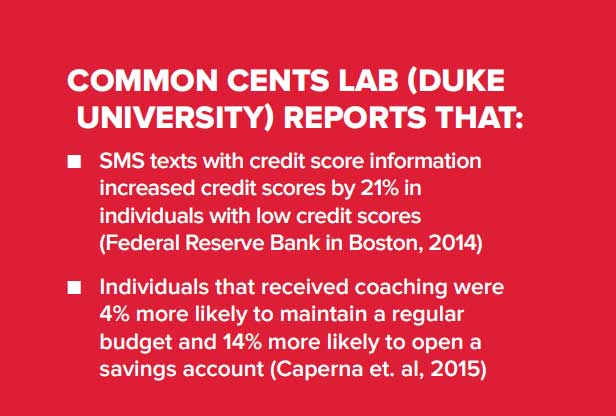

There is also ample evidence, dating back to 2013 that intervention helps employees make better investment decisions (auto enroll, escalate, etc.) Time-sensitive, compressed, outcome-driven, multi-channel participant communications and education campaigns structured as step-by-step instructions convey a sense of urgency and are more effective at driving behaviors and outcomes.

Is there a risk that the old-fashioned approach to 401(k) plan education might actually deter participant action? There is evidence that this may be the case. In a research paper titled “Subjective Knowledge in Consumer Financial Decisions”, the authors (Liat Hadar, Sanjay Sood, and Craig R. Fox of the Anderson School of Management at UCLA) propose that effective financial education must focus not only on imparting relevant information and enhancing Objective Knowledge (how knowledgeable they are) but also on promoting higher levels of Subjective Knowledge (how knowledgeable they feel) because increasing savers’ objective knowledge regarding financial instrument can actually deter their willingness to invest1. So, do context and confidence play a role in participant action?

In a research report titled “Financial Literacy, Financial Education and Downstream Financial Behaviors”, Daniel Fernandes of the Rotterdam School of Management of Erasmus University, John G. Lynch, Jr. of the Leeds School of Business of University of Colorado-Boulder, and Richard G. Netemeyer* of McIntire School of Commerce, University of Virginia, Charlottesville conclude that interventions to improve financial literacy explain only 0.1% of the variance in financial behaviors2. They suggest a reduced role for financial education, and a real but narrower role for “just-in-time” financial education tied to specific behaviors it intends to help.

The pandemic and other recent events has highlighted how prepared (or not) Americans are to withstand financial crisis has led to increasing demand by sponsors and employees for holistic Wellness Programs available to employees when and where they want to receive it—in other words on -demand or just-in-time.

At the time of need, participants can be directed to the content most relevant to their specific situation. The key to success is the ability to connect with participants individually and to address their personal situation with relevant content just when they need it. Technology is the enabler.

employees for holistic Wellness Programs available to employees when and where they want to receive it—in other words on -demand or just-in-time. At the time of need, participants can be directed to the content most relevant to their specific situation. The key to success is the ability to connect with participants individually and to address their personal situation with relevant content just when they need it. Technology is the enabler.

Part of the participant experience on which the plan sponsor needs to reflect is permissions – notifications on the app or SMS / Text permission. Participants are in control of the permission – “Opt-out” in “Automatic enrollment” means something different now. With an app, participants are in control of the notification settings. In notification settings, they can make a distinction between administrative notifications and information notifications – “Your profile” is now an expanded profile including preference elections.

Does just-in-time reflect an omni -channel approach or is it digital or in-person only? Does it have to be a binary choice? Or will the digital transformation currently underway drive a more meaningful in-person experience.

- Subjective Knowledge in Consumer Financial Decisions – Journal of Market Research - Vol. L (June 2013), 303–316

- Financial Literacy, Financial Education and Downstream Financial Behaviors - 2014

Final Thoughts and Conclusions

It is arguable that just- in-time and on-demand participant education and coaching campaigns are effective at driving participant behaviors and outcomes. With the increasing access to and control over information held by individuals, it is possible that change, including disruptive change, is imminent. The current environment begs many questions.

For example, Average Joe investors, coordinated on Reddit, roughly quadrupled the stock price of the struggling video game retailer GameStop (GME) in a trading frenzy that has cost traditional Wall Street hedge funds millions of dollars. This same Average Joe is also contributing to his retirement plan at work. So, what has he learned through this increasing control and access?

Robinhood, Webull, TradeStation, SoFi Active Investing, TD Ameritrade, ZIGGMA and others are bringing trading, analysis, evaluation and expanded brokerage services for lower fees and in a format that capitalizes on the changing sensibilities of investors. What will these developments mean for retirement plans? What about crypto currencies, like bitcoin? Will those slowly make their way into retirement plan investment menus? 401K Specialist Magazine asks, “While 401k participants might not be banging down the door of their plan sponsors to provide access to bitcoin investing today, who’s to say tomorrow’s plan participants—once some fiduciary, security and regulatory barriers are cleared—won’t be?”

Technology is influencing today’s retirement plan investors and so is their age. The workforce is getting younger. The oldest members of Gen Z are 24 years old and have entered the workplace. Generation Z prefers to play video games, stream music, and engage on social media. What is the best approach to effectively drive saving and investing behavior with this cohort?

Millennial employees—those turning 25-40 this year—are now the largest segment of the workforce, according to Pew Research. These digital natives are using their sway to drive technological change that makes work more efficient. CompTIA’s research, for example, shows that two-thirds of millennials and their younger Gen Z colleagues—those turning 23 and younger—consider an organization’s embrace of technology and innovation as an important factor when choosing an employer. What does that mean for the retirement services industry when it comes to attracting and retaining talent let alone driving effective participant behaviors and outcomes.

The challenge remains then- how best to drive participant behaviors and outcomes in a way that will help Americans be prepared for retirement. What then is the next, best approach?

Retirement plan service providers, advisors and even plan sponsors will have to be nimble and be willing to take risk to avoid simply reacting to the rapidly changing world of personal, personalized, customized, on-demand communications. Knowledge and confidence appear to be critical attributes of participants who acted and, as a result experienced better retirement outcomes. That information may be the keystone of future communication programs and efforts. What will that look like? Success may be measured by those retirement plan service providers, advisors and sponsors who are willing to take a risk and find out.

JUST-IN-TIME AND ON-DEMAND COMMUNICATIONS ARE CERTAINLY MORE EFFECTIVE THAN ARE THE PAPER-BASED MASS COMMUNICATIONS OF THE PAST

3 “Modern Learning: 6 Reasons Why Learning Has Changed Forever,” elearningindustry.com, 6/21/16.

4 John Hancock’s sixth annual financial stress survey, John Hancock and Greenwald & Associates, 2019.

About the 401(K) Listening Post

The 401(k) Listening Post is “Where you voice ideas and service providers listen”. The post provides a venue for sponsors of defined contribution retirement plans and their advisors to voice ideas and suggestions to enhance the retirement readiness and financial wellness of working Americans. Suggestions and ideas are shared with retirement plan service providers at industry meetings. The 401(k) listening post accomplishes its mission through an open and honest feedback mailbox, periodic surveys and interviews. In turn, participating retirement plan service providers share their thought leadership, news, and industry initiatives to help plan sponsors and advisors advance the success of their retirement plan.

For questions regarding this publication, contact:

Eric Henon, Executive Director

The 401(k) Listening Post

16 A Pasco Drive | East Windsor CT 06088

information@401klisteningpost.com

+1.860.254.5046